Six Assumptions and Facts about California’s Proposed SAF Credit

The Sustainable Aviation Advisory Council finds the debate about the SAF credit in the California Governor’s 2026-27 budget somewhat one-sided at this point. We believe that the UC Berkeley Haas blog and the Legislative Analyst’s Office (LAO) report fundamentally missed the mark with questionable assumptions and a lack of understanding of how markets and supply chains respond to shifts in supply. As a non-partisan advisory council with an educational mission, we feel compelled to contribute to the ongoing policy debate with the following short list of assumptions and facts. For a more robust invitation to respond to questions, please see our website: https://www.safadvisory.org/.

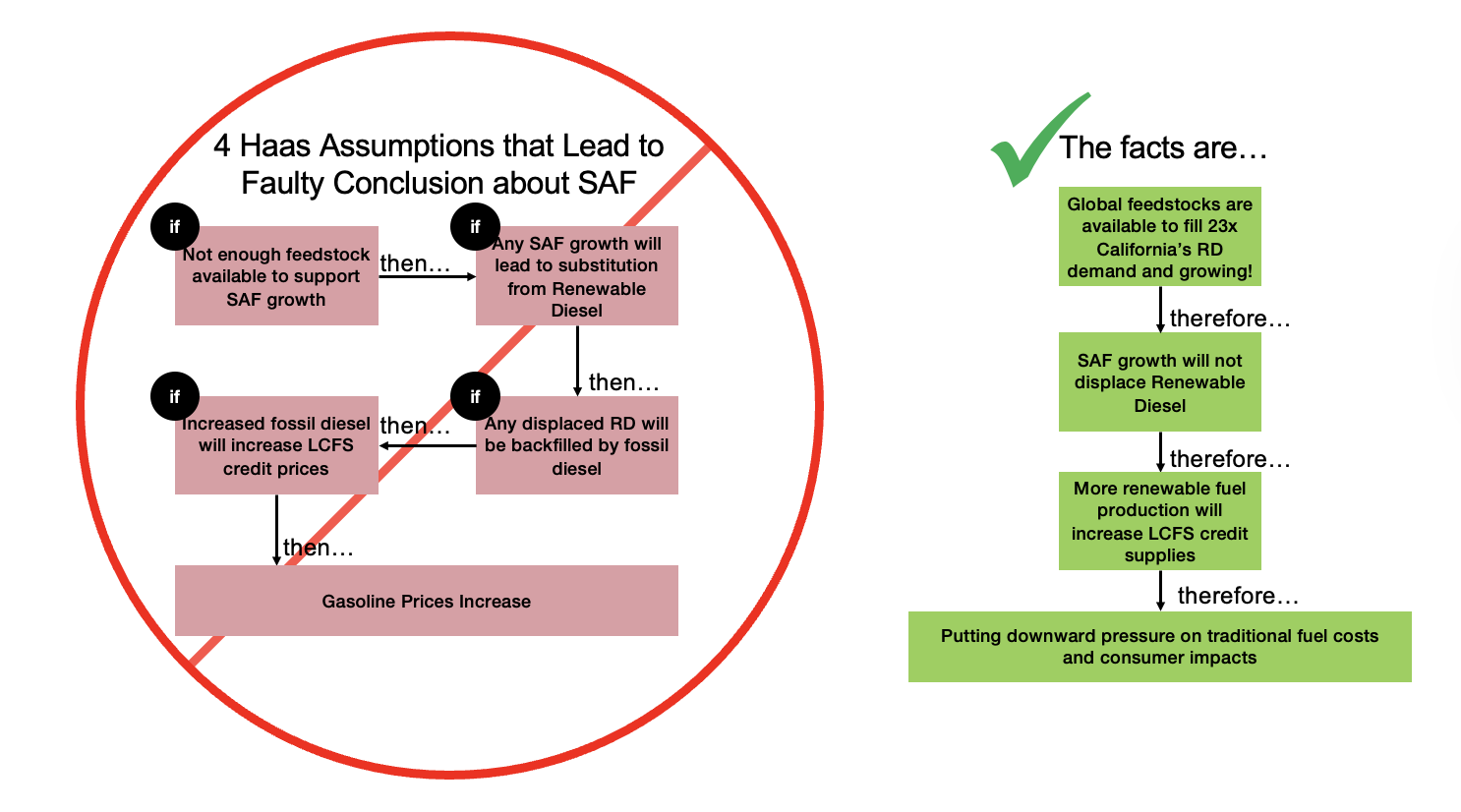

Assumption #1: “The SAF credit will significantly raise gasoline prices.”

Fact: This is inaccurate. This conclusion relies on a model that assumes renewable fuel producers are maxed out to full capacity, and if a facility were to produce more SAF, they would produce less renewable diesel. This is not correct. In reality, U.S. renewable fuel producers are running 40% under capacity. They have room to increase production of renewable fuels, which in turn will put downward pressure on Low Carbon Fuel Standard (LCFS) prices. Additionally, displacing fossil aviation fuel with SAF frees up refinery and market capacity to increase gasoline supplies, putting downward pressure on gasoline prices.

Assumption #2: “There is not enough feedstock to support both renewable diesel and SAF production.”

Fact: This is incorrect. This is the same argument that was used in 2022, before several new renewable fuel production facilities came online (mostly in California) and almost doubled US production capacity. According to the Advanced Biofuels Association[1], the global supply of eligible feedstock is currently over 5.9 million barrels per day (90 billion gallons) – almost 23 times the diesel demand of California. The global collections rates of used cooking oil are less than 10%, so the availability of renewable feedstocks will likely continue to increase as long as economic incentives remain stable.

Assumption #3: “Renewable diesel refineries can easily switch to producing SAF.”

Fact: This is false. Producing jet-quality renewable fuels requires tighter process control and additional refinery investment. Converting a facility optimized for renewable diesel into SAF production is neither automatic nor inexpensive, which limits the large-scale diversion assumed in the Haas and LAO analyses.

Assumption #4: “SAF policies don’t meaningfully reduce emissions.”

Fact: This is incorrect. In fact, SAF has the highest ROI for addressing climate goals in the aviation sector by immediately reducing lifecycle carbon emissions, particulate matter, and other harmful greenhouse gases, without requiring new infrastructure. It benefits local air quality leading to health benefits for vulnerable communities. Additionally, there are no good options to decarbonize aviation. Batteries are too heavy for long-haul aircraft and hydrogen faces major infrastructure challenges. Sustainable aviation fuel is the only scalable pathway to reduce aviation emissions over the coming decades.

Assumption #5:“The SAF credit would cost the state more than $1 billion per year.”

Fact: The estimate from the LAO report assumes far more SAF production capacity (834 million gallons) than currently exists in the U.S. (460 million gallons)[2] and further assumes rapid conversion of RD refineries (see Assumption #3). When realistic production and logistics constraints are considered, the potential fiscal exposure to California’s budget appears substantially lower.

Assumption #6: “California can’t reduce global GHG emissions by acting alone.”

Fact: Nearly every climate policy implemented at the state level faces some degree of market and emissions “leakage”. California’s clean fuel policies – like LCFS and cap-and-trade – operate within a global energy system and yet still have successfully driven the expansion of overall low-carbon fuel supply. Despite its small contributions to reducing global GHGs, California’s leadership on decarbonization has already created real-world impacts on markets and technologies at a global scale.

References

[1] ABFA estimates total global renewable fuel feedstock supply in 2024 was 5.9 million barrels per day (294 million metric tons) https://advancedbiofuelsassociation.com/wp-content/uploads/2025/07/ABFA-Feedstock-Study-2025.pdf

[2] https://www.eia.gov/todayinenergy/detail.php?id=65204